Top things that make craft beer bars, bottle shops and distilleries insurable (and uninsurable)

By David DeLorenzo

The hospitality industry is big business. The National Restaurant Association reported in February of this year that in December 2025 alone, “eating and drinking places” registered total sales of $100.2 billion on a seasonally adjusted basis, with a fourth quarter outcome topping $300 billion. The organization calls this sector “the primary component of the U.S. restaurant and foodservice industry.”

But often with great reward comes great risk. In 2025, the National Restaurant Association estimated 30% of bars and restaurants fail in the first year. While thin margins and stiff competition are among the reasons these types of establishments quickly close up shop, another main reason is complex operational demands.

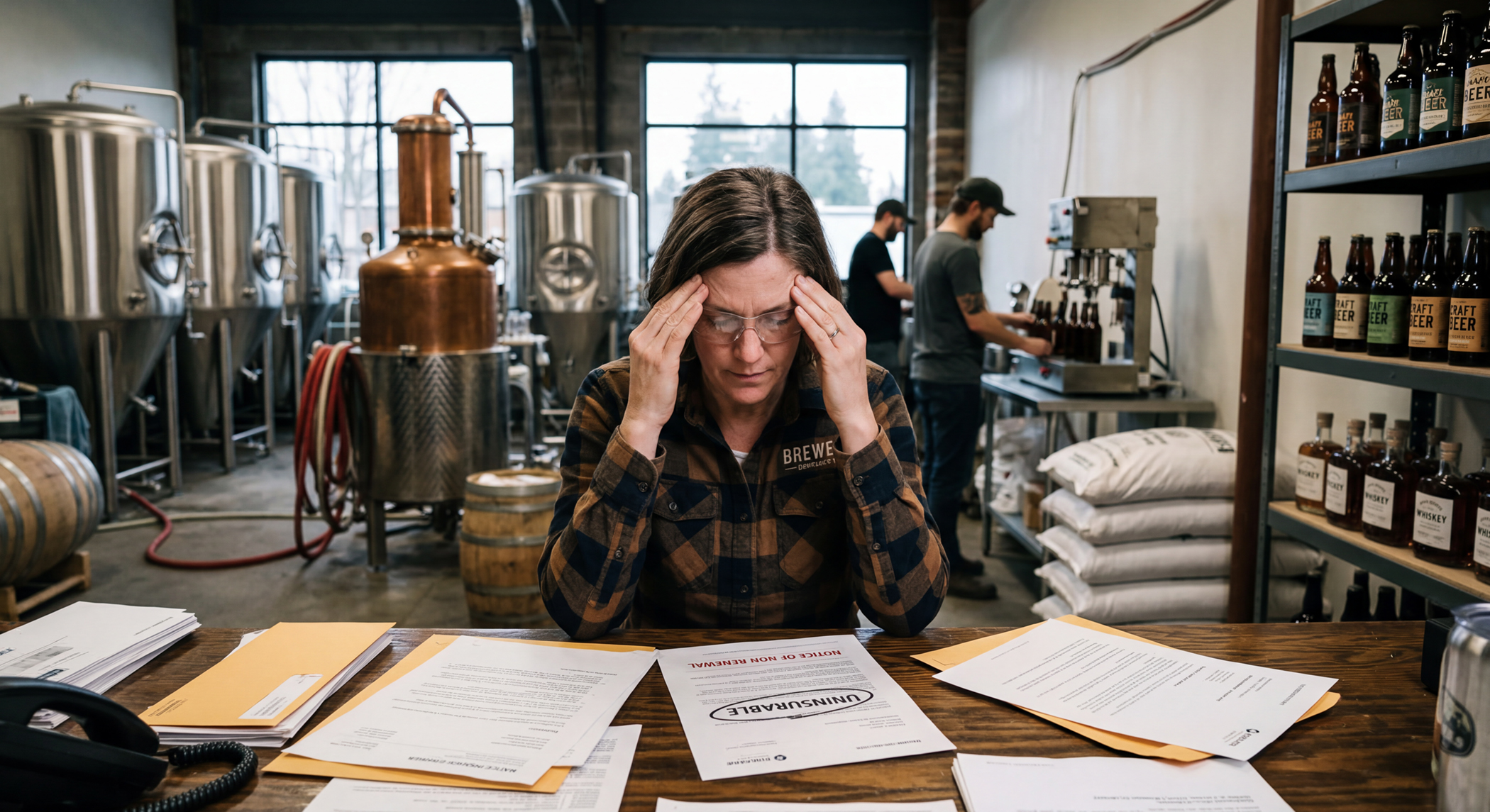

While craft beer brewers and fine spirits developers may be passionate about their craft, they may not be well-educated on the business end of, well, business. Particularly when it comes to licensing and insurance, craft beer breweries, distilleries and other establishments making and serving liquor need to know the ins and outs of what makes them insurable — and more importantly, what doesn’t.

Being properly licensed and insured is an absolutely critical factor to the success of any business, particularly in the hospitality industry. This article focuses the lens on insurance and what insurance carriers are looking for. An establishment can end up paying a lot more for its premiums or be locked out of an insurance policy altogether, and it comes down to best practices.

There are three major components that insurance carriers are looking at when it comes to covering a policy for establishments like craft beer bars, bottle shops, distilleries and other places that serve liquor. The “big three” are the amount of liquor or beer volume being served, entertainment, games and late hours, and procedures for overserving prevention, training and documentation.

The amount of liquor or beer volume being served: The percentage of alcohol sales is a defining factor when it comes to insurance. Exposure is a definitive factor when it comes to how much an establishment should expect to pay for its coverage. For example, a restaurant with 10% liquor sales will very likely pay less than a bottle shop with 40% liquor sales or more. In addition to the liquor sales, the industry category will also have an impact on rates. This is due to the risks that the business encounters. Rates will vary based on the risk that the insurance carrier expects to take on with any given business that serves alcohol.

Entertainment, games and late hours: They say nothing good happens after midnight. And while there may be some debate on that, depending on who’s at the receiving end of that sentence, when it comes to insurance companies, late nights are a red flag. This comes down to the fact that the longer patrons linger in a place serving alcohol and the more they order, the more likely they are to become intoxicated and therefore a risk to the establishment, to themselves and to others. Late-night happy hours or last-call specials offered by establishments may also be looked at as a red flag. It could be construed as “encouraging” patrons to drink up as it gets closer to closing time, when they will then potentially get in their cars to drive home — big red flag.

Entertainment and games could also impact rates and coverage, once again, based on the risk that the insurance carrier is willing to accept. Certain entertainment and games hold less risk than others, depending on their nature.

Procedures for overserving prevention, training and documentation: Poorly or undocumented procedures, negative culture in the employee environment and lack of experience can be indicators that will make an insurance carrier turn away. Another big red flag is if an establishment has claims that are open or have reserves on them. This makes it extremely difficult for a new carrier to want to write the coverage on it.

Having proper training and procedures in place is one of the most important things an establishment serving liquor can do to enhance the safety of staff and patrons, to mitigate their risk for getting caught up in a lawsuit and also to obtain reasonable insurance rates.

Risks that establishments serving alcohol face: No matter how it’s looked at, liquor liability will always be a challenge that establishments serving alcohol will face, regardless of the state in which they are operating. However, that is not where the risk ends. There are also lesser-known or not-often-considered liabilities including product liability, contamination of product or product recall. There are risks such as fire or explosions from open flames and vapors, particularly in distilleries. Equipment breakdowns can cause a major business interruption and losses.

Best practices to become more insurable: The number one thing a business can do to keep its insurance rates lower is invest in safety protocols and meticulous standard operating procedures. The fewer claims businesses have and the more they can prove to the carrier that they run professional operations that abide by the rules, the more “insurable” they become. Some standard operating procedures to consider include.

Document it: Having air-tight documentation records and licensing is vital for any business, whether they are serving alcohol or not. But it is even more important for those who do. Documentation and licenses should also be easily accessible if they are needed in an instant.

Record it: Security and video footage are also crucial. Having a time-stamped video can be the very thing that protects a business if a lawsuit arises.

Train them: Keep excellent, well-documented records of employee training with alcohol, from service to batch tracking and other procedures regarding alcohol. For example, instill strict policies on checking IDs and make sure employees are educated on determining if a patron is perhaps already inebriated before serving them any alcohol. Make it common practice never to overserve anyone.

Clean it up: This goes beyond the physical appearance of the establishment. Owners should take care of how they are presenting themselves through their website, social media, branding and marketing. If the online presence looks disheveled and disorderly, the underwriter will assume that of the business itself and may be hesitant to cover a business for that reason. This also goes for the entertainment and experiences being promoted. Offering crazy activities in an attempt to attract new customers may end up costing establishment owners by way of higher rates or none at all.

Out of his passion for serving the restaurant and hospitality industry, David DeLorenzo created the Bar and Restaurant Insurance niche division of his father’s company, The Ambassador Group, which he purchased in 2009. For more than 20 years, he has been dedicated to helping protect and connect the hospitality industry in Arizona. For more: barandrestaurantinsurance.cohttp://www.barandrestaurantinsurance.comm.